On Friday, 27 February 2026, the European Commission announced its intention to apply the trade agreement with Mercosur countries Argentina and Uruguay on a provisional basis. In doing so, it is not waiting for the verdict of the EU Court of Justice. That court, at the request of the European Parliament, still has to assess the agreement's compatibility with EU law. Brazil and Paraguay are also expected to ratify the treaty soon.

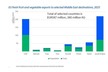

The trade relationship between the European Union and the South American Mercosur bloc is often discussed in terms of cars, soy, or beef. Less visible, but also relevant, is the exchange of fruit and vegetables. Looking at the preliminary 2025 trade figures for fruit and vegetables (source: Eurostat), the picture for the EU remains clearly negative.

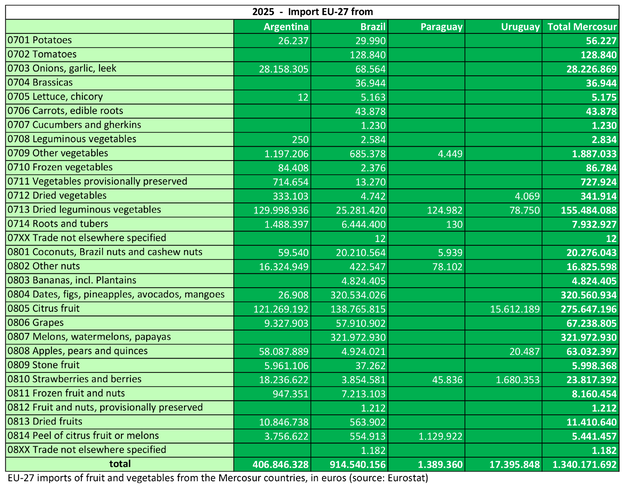

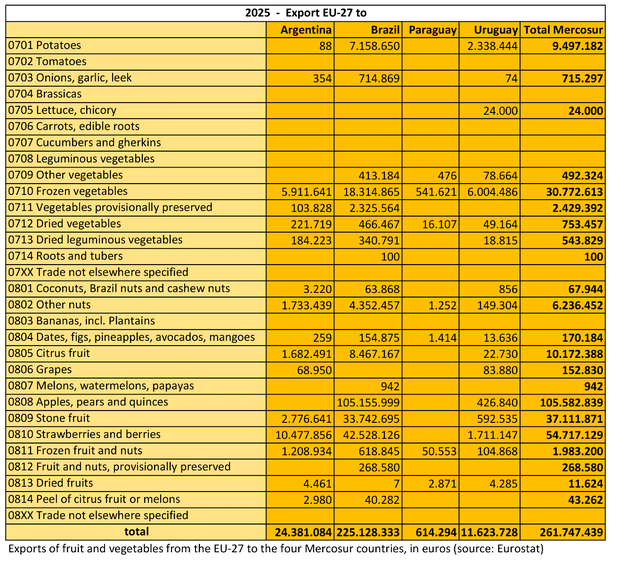

Based on Chapter 07 and 08 customs classification totals, the EU-27 will export €261.7 million worth of fruit and vegetables to the four Mercosur countries combined in 2025. In the opposite direction, the EU imports €1.34 billion from Mercosur. In balance, this means a negative trade result of €1.078 billion for the EU. The deficit is mainly in fruit, nuts, and dried fruit: Chapter 08 accounts for €216.5 million in EU exports, compared with €1.145 billion in imports. In vegetables (Chapter 07), the gap remains smaller, but still substantial: €45.2 million in exports against €195.0 million in imports.

Brazil as a hub

Brazil is the hub of trade. On the export side, about 86% of all EU shipments of fruit and vegetables go to Brazil: €225.1 million out of a total of €261.7 million. Argentina follows well behind with €24.4 million, Uruguay with €11.6 million, and Paraguay with barely €0.6 million. On the import side, Brazil's dominance is slightly less absolute but still decisive, supplying €914.5 million, or over 68% of all Mercosur exports to the EU. Argentina is a much heavier second player here than on the export side, with €406.8 million, or over 30% of the import value. Uruguay (€17.4 million) and Paraguay (€1.4 million) remain relatively small.

Looking at EU member states, exports are highly concentrated in a limited number of countries. Spain is the largest European exporter to Mercosur in 2025 with €78.9 million, followed by Italy with €67.8 million and Portugal with €51.4 million. Together, these three countries already account for three-quarters of total EU exports. They are followed by Greece (€28.9 million), Belgium (€18.0 million), and the Netherlands (€11.0 million). Other member states play a much smaller role; in several central and eastern European member states, exports are almost negligible. On the import side, the pattern is even more skewed: the Netherlands acts as the gateway with €701.2 million, more than 52% of all EU imports from Mercosur in these product groups. This is followed by Spain (€258.6 million), Italy (€130.7 million), and Portugal (€114.0 million). Germany, France, Greece, and Belgium form a second group, but at significantly lower levels.

Vegetables

In the vegetable trade, the EU deficit remains mainly an Argentinian story. Of the total EU imports of €195.0 million in Chapter 07, €162.0 million came from Argentina. Brazil still supplies €32.7 million; Paraguay and Uruguay are marginal here. On the export side of vegetables, Brazil is actually the main outlet: €29.7 million of European vegetable exports go there. Uruguay follows with €8.5 million, Argentina with €6.4 million, and Paraguay with €0.6 million.

Interestingly, European vegetable exports are strongly supported by north-western Europe: Belgium alone accounts for €17.5 million, or almost 39% of all EU vegetable exports to Mercosur. The Netherlands follows with €10.5 million and Spain with €10.4 million. This indicates an export profile in which frozen vegetables (peas, spinach, mixes, and other vegetables) carry significant weight (€26.44 million). This is followed by seed potatoes with €9.48 million. Of these, most go to Brazil (€7.14 million) and Uruguay (€2.34 million).

On the import side of vegetables, the product mix is quite different. The largest item is brown beans (€114.6 million). Almost that entire amount comes from Argentina (€92.6 million), with Brazil supplying €22.0 million. This is followed by garlic at €28.0 million, almost entirely from Argentina, and chickpeas at €27.3 million, again almost entirely Argentinian. Also relevant are sweet potatoes (€7.08 million) and onions (€5.60 million). In vegetables, the EU therefore mainly imports bulk products and basic commodities from Mercosur, while exporting more processed or logistics-intensive products.

© FreshPlaza

© FreshPlaza

Fruit

In fruit, the difference is even more pronounced. EU exports of fruit to Mercosur amount to €216.5 million, while imports reach €1.145 billion. Within those fruit imports, Brazil is dominant with €881.8 million, accounting for about 77% of all Mercosur fruit to the EU. Argentina follows with €244.8 million, while Uruguay (€17.3 million) and Paraguay (€1.3 million) remain small. On the export side, €195.4 million of European fruit exports go to Brazil. In other words, almost the entire fruit relationship between the two blocs revolves around European sales to Brazil and European supplies from Brazil and Argentina.

European fruit exports are supported by a relatively limited number of highly competitive product lines. The largest export item is apples, with €77.6 million. Of this, €77.5 million goes to Brazil alone. Within the EU, Italy (€45.5 million) and Portugal (€22.1 million) are by far the main suppliers, followed by Spain and France. The second largest item is kiwis with €50.3 million. This product is mainly supplied by Greece (€28.9 million) and Italy (€17.9 million), with Brazil the biggest destination and Argentina second. This is followed by plums with €30.7 million, pears with €27.9 million, and peaches/nectarines with €6.4 million.

© FreshPlaza

© FreshPlaza

At the same time, imports from Mercosur show where the European dependence lies. By far the largest item is mangoes and related fruits at €286.6 million, practically all from Brazil. The Netherlands is the central European hub here with €182.3 million, followed by Spain (€60.5 million) and Portugal (€29.1 million). Next come lemons and limes with €243.6 million. This product comes from both Brazil (€138.8 million, especially limes) and Argentina (€99.2 million, especially lemons), with the Netherlands again the largest importing member state. The third largest item is melons with €169.8 million, all from Brazil. Next, we see papayas with €86.4 million, watermelons with €65.8 million, and grapes with €57.9 million, all leaning heavily on Brazil. In addition, pears (€45.6 million, almost entirely from Argentina), oranges (€30.8 million), avocados (€26.3 million), and soft fruit (€14.8 million) also remain relevant import lines.

Overlapping codes

It is precisely in some overlapping codes that it becomes clear where competitive relationships really lie. The EU has a clear surplus in apples in 2025: €77.6 million in exports versus €17.5 million in imports, i.e., a positive balance of over €60 million. Europe is also strong in kiwis (+€46.4 million) and plums (+€30.6 million). But that does not offset the heavy negative balances in tropical and subtropical fruits. In mangoes, the EU deficit reaches almost €286.6 million. In lemons and limes, the deficit is €243.2 million. In melons, it is €169.8 million, and in papayas, €86.4 million. Even in products in which the EU itself has an export position, such as pears and oranges, the balance remains negative due to large import volumes from Argentina, Brazil, and Uruguay.

Geographically, southern Europe (Spain, Italy, Portugal, and Greece) dominates European exports to Mercosur. North-western Europe, with Belgium and the Netherlands leading the way, plays a relatively heavier role in vegetables and in logistics-driven, processed flows. On the import side, the Netherlands is the central hub for transit and distribution within the internal market, especially for fruit. On the Mercosur side, Brazil mainly supplies tropical fruits and melons, while Argentina has a much stronger position in pulses, garlic, citrus, and pears. Uruguay is a modest but visible citrus supplier. Paraguay remains statistically small in this trade in 2025.