Growth in seaborne perishable cargo slowed in 2019 but is forecast to better weather the COVID-19 induced economic storm than the dry cargo trade given the broader resilience of the food supply chain. Meanwhile, availability of refrigerated container equipment is forecast to tighten as buoyant trade and continued modal shift boost expansion in reefer cargo carried by containerships, according to Drewry’s latest Reefer Shipping Annual Review and Forecast 2020/21 report.

Worldwide seaborne reefer trade recorded growth of just 1.7% in 2019 to 130.5 million tonnes, its weakest rate of growth since 2015. Traffic growth was held back due to lower shipments of both deciduous and citrus fruits on the back of extreme weather conditions in Europe and drought in South Africa and Chile, though aided by soaring pork traffic into China following the outbreak of African swine fever.

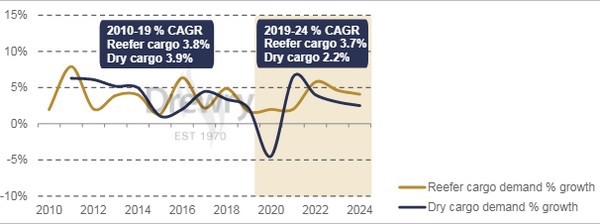

Drewry forecasts that seaborne reefer traffic will reach 156 million tonnes by 2024, representing average annual expansion of 3.7% which is faster than the anticipated growth in the wider dry cargo trade (see chart).

“Drewry expects the reefer trade to be more recession proof against the economic impacts of COVID-19,” said Drewry’s head of reefer shipping research Philip Gray. “And near term, it will continue to benefit from African swine fever induced protein demand into Asia. The continuing trade standoff between the US and China remains a threat to transpacific trade, but could provide opportunities on other routes through trade substitution, such as East Coast South America to Asia.”

Refrigerated reefer cargo demand development compared to dry cargo demand

Source: Drewry’s Reefer Shipping Annual Review and Forecast 2020/21

Meanwhile, reefer traffic continues to shift from the dwindling specialised vessel mode to fully cellular containerships. Drewry estimates that the former’s share slumped to 13% in 2019 and is projected to diminish further to just 8% by 2024, due to an ageing fleet and limited investment in newbuilds. Bananas and fish are the biggest commodities carried in specialised reefer ships and their largest trade route is West Coast of South America to Europe thanks to the dominance of the banana trade out of Ecuador.

By contrast, buoyant trade growth and modal shift have enabled reefer container cargo growth to fast outstrip that of the wider container shipping market. As a consequence, the volume of reefer cargo carried by the world’s fleet of containerships expanded 3.4% in 2019 to 5.3 million feu. And this trend is set to continue, with Drewry forecasting average annual containerised reefer growth of approaching 5% in the period to 2024, far outstripping that of dry the container trade.

“However, availability of refrigerated shipping container equipment remains a challenge, due to the highly imbalanced nature of reefer trade routes,” added Gray. “And Drewry expects conditions to tighten as equipment fleet growth is not expected to keep pace with projected cargo demand.”

Based on analysis of the top 15 reefer trade routes covered in the report, Drewry estimates that global deep sea reefer trades are 82% imbalanced, with major exporting regions such as South and Central America, Oceania and Southern Africa limited by particularly high negative imbalance ratios.

For more information:

Drewry

Tel: +44 20 7538 0191

www.drewry.co.uk