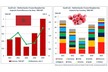

The UK sweet cherry category enters the 2026 season on the back of structural growth, improving agronomy, and sustained retail demand. Production has stabilised at a materially higher baseline than five years ago, with annual output having the potential in the 9,000 tonne range in favourable seasons.

"However, this is still a supply-constrained, premium category, with domestic fruit prioritised for high-value channels," explains Jon Clark, Managing Director at Fruit World International. "The strategic opportunity for growers, particularly through partners such as Fruit World International, remains in optimising non-retail routes (export and wholesale) to manage peak volumes and maximise returns."

Production overview – structural position of the UK cherry sector

The UK cherry industry has undergone a quiet transformation, with a transition to high-density, protected orchards (polytunnels), which has improved yield reliability and fruit quality, and the expansion of self-fertile, larger, firmer varieties has extended the season and retail appeal.

The UK season now runs from early June to late September.

"Despite this progress, domestic production still represents a minor share of total UK cherry consumption, with imports dominating outside the domestic window, with the UK consuming around 16,000t of sweet cherry in the April to September period. The category remains weather-sensitive, with yield variability depending on spring conditions. Assuming average weather, production in 2026 is likely to settle slightly below the exceptional 2025 peak but remain structurally strong. The forecast for the 2026 UK sweet cherry crop is 8,000 tonnes."

© Fruit World International Ltd

© Fruit World International Ltd

Key Growing Regions and Contribution

Production in the UK was traditionally in Kent, known as the "Garden of England" and also the place where Henry VIII first planted commercial cherry trees in the UK, but over the last two decades, production in other areas, most notably Herefordshire and Scotland, has increased volumes and extended seasons.

UK production is concentrated in a number of specialist regions:

South East (Kent & South East England) represents around 60% of the UK volume, the West Midlands (Herefordshire, Staffordshire & Worcestershire) accounts for around 25%, and is expanding the commercial base with modern orchards as well as extending the season from the start of June until late August with a strong mid-season supply.

East Anglia (Norfolk, Suffolk, Cambridgeshire) grows around 5% of the UK's cherries. The region is a rapidly developing region with new plantings, benefiting from lighter soils and irrigation control, and can produce fruit from the beginning of June.

Scotland supplies the UK market later in the season with around 10% of the total production. This extends UK availability into August/September, which is critical for maintaining UK shelf presence after southern production stops.

© Fruit World International

© Fruit World International

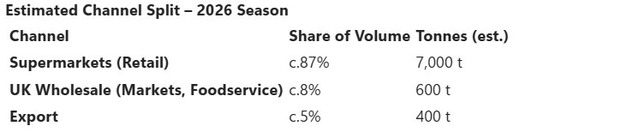

Market channel distribution (2026 Forecast)

"The UK cherry market is retail-dominant, and although Fruit World International is involved in the non-retail, we stress the importance of having a strong domestic retail business, but also to have the ability to develop other areas to balance the marketing and bring a more balanced option to seasonal supply challenges and opportunities."

© Fruit World International

© Fruit World International

"In 2026, retail remains the anchor, but not the long-term solution for peak volume or early and late season opportunities that present themselves locally and globally. Developing varieties as well as pre and post-harvest management of cherries not only benefits the retail business but also presents more opportunities to have the right fruit in the right market to deliver value for all.

"The UK wholesale markets with strong brands like Blossom and Bonanza, supported with great fruit offers a different outlet for growers, and this also opens up export opportunities with Fruit World International, supplying a number of customers across the EMEA region. Customers in these regions often take pack formats that help growers become more efficient in their cost per kilo to pack and transport. It is not all easy work, though; this also presents a number of challenges, which is why Fruit World International focuses on cherries only during the season. I believe alongside the domestic retail and scaling in these new markets, farms are securing their financial future and gaining the momentum to increase their production area."

© Fruit World International

© Fruit World International

Strategic Insight – The Role of Market Diversification

"This is where the philosophy associated with Fruit World International becomes critical. The UK cherry industry's structural challenge is not production; it is market concentration. Retail programmes front-load value but cap volume. The peak season (July) regularly produces short-term oversupply, and without alternative routes, growers are forced into discounting, suboptimal picking decisions, and waste.

"The value of non-retail channels is a diversified route-to-market strategy which delivers price resilience, full crop utilisation and improved grower returns across the whole season."

2026 season outlook

The UK sweet cherry sector in 2026 is no longer a niche; it is a sophisticated, high-value category with structural momentum, according to Jon.

"However, the commercial success of the crop will increasingly depend on how it is sold, not just how it is grown. Growers aligned with integrated marketing partners offering retail, wholesale, and export capability alongside category insight will outperform those reliant on a single route to market. That is the difference between selling cherries and managing a cherry business."

For more information:

Jon Clark

Fruit World International

Tel: +44 (0) 7525 668880

[email protected]

www.fruitworld.co.uk