AHDB overview of 2017 potato trade

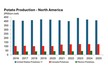

The AHDB analyst explains that potato production was lower year-on-year across the NEPG countries (NL, B, FR, GB, and DE). At 5.2Mt, the total GB potato crop was the fourth-smallest on records going back to 1960. The total NEPG crop (excluding seed and starch) was the smallest since 2013, although this comes against a rising trend with demand for raw material in Belgium and the Netherlands continuing to grow, according to AHDB data.

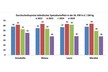

“This has already meant a generally tight supply situation, with prices rising in response. The main indication of whether supplies are continuing to tighten will be from how stocks levels develop,” Marshall continues. However, as the prices consolidate across the NEPG, they suggest that the tighter supplies and higher prices will affect most of these countries.

Many processors, both in GB and elsewhere in the NEPG, source the majority of required supplies on contract, and this continues to be the main way to manage volatility in both price and yields. Supply chains tend to be well integrated which, helps processors to ensure that they are able to source the right amount of the crop, as Marshall explains. Recent trends in GB plantings have included a shift towards newer, high-yielding, processing varieties with lower levels of waste.

Until we know the details of any deal that may be made, it is too early to be able to tell what the eventual impact of Brexit may be on potato prices.

“We do know that the vote and subsequent speculation about the nature of the deal weakened the pound. This meant that, for a short period in October, GB prices for processing material became noticeably cheaper than continental values, although, since then, the weaker pound has contributed to the rising prices in GB.

source: potatobusiness.com