Widespread container shipping trade recovery in the wake of the Covid-19 pandemic has boosted the global terminal capacity outlook, supported by global terminal operators’ (GTOs) increased appetite for higher-risk greenfield projects to deliver long-term growth, according to Drewry’s latest Global Container Terminal Operators Annual Review and Forecast report.

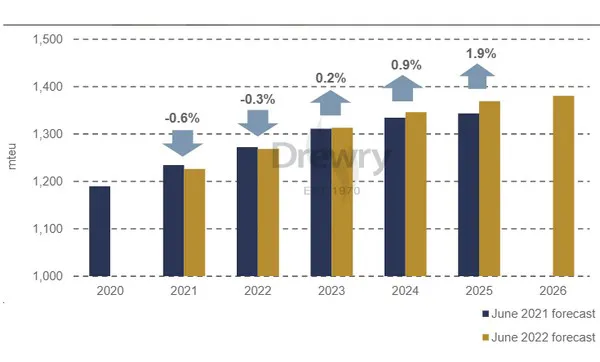

Global container port capacity is projected to increase by an average annual rate of 2.4% to reach 1.38 billion teu by 2026. However, the worsening economic and geopolitical situation has led to a downgrading of the cargo demand outlook, and as a result container port utilisation is now projected to moderate to 70% in 2025 compared to last year’s projection of 75%.

While the majority (70%) of GTO investment plans remain focussed on existing assets, there has been a notable increase in the number of greenfield projects – with CMA Terminals, Hutchison and TIL all expected to add 4m teu or additional greenfield capacity by 2026.

Eleanor Hadland, author of the report and Drewry’s senior analyst for ports and terminals said: “The renewed appetite for greenfield projects shows improved confidence in the market outlook. However, the ability of CMA Terminals and TIL to secure volume guarantees from CMA CGM and MSC gives these companies an advantage over non-carrier affiliated operators.”

Global supply chain disruption resulted in increased cargo dwell times in 2021 which generated additional storage charges, lifting terminal operators’ revenue growth above that which could be justified on the basis of volume recovery alone.

Port congestion does not appear to have adversely impacted financial performance, despite the widespread decline in productivity levels. The revenue raising mechanisms (i.e., paid-for overtime, storage charges) have so far proven to be sufficient to offset the additional congestion-related operating costs. Operators also cite the continuing cost control measures implemented in response to Covid as having a positive impact on margins.

“Once global supply chain disruption eases, which is now expected in 1H23, there is heightened risk that revenue gains will retreat as dwell times return to pre-pandemic levels,” added Hadland.

Capital expenditure bounced back in 2021, rising 31% YoY, but operators now face the twin challenges of longer lead time for handling equipment and rapidly rising costs. Drewry’s research also identifies that the pace of fund raising has slowed since 2020, with rising interest rates putting a brake on the market. In general, favourable terminal operator financial performance has translated into robust balance sheets. With the exception of COSCO Ports and ICTSI, net debt fell, leading to a reduction in net gearing by 8.5 percentage points to 54.7%.

Looking back at 2021, the number of companies that qualified as GTOs fell from 21 to 20, with K Line dropping out of the rankings following the sale of its US operations in 4Q20.

For more information:

Eleanor Hadland

Drewry

Tel.: +44 (0)20 7538 0191

hadland@drewry.co.uk

drewry.co.uk