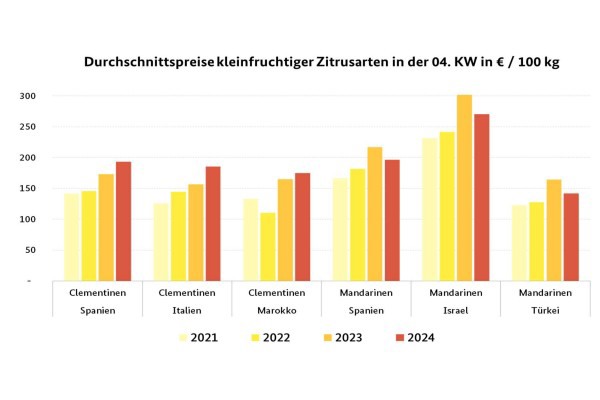

The significance of mandarins has evidently grown: In addition to Spanish Clemenvilla, Clemenova, and Tango, Nadorcott has also been received. Offers from Spain were not always convincing in terms of quality, resulting in occasional price reductions. Israeli Orri, on the other hand, had no issues with quality, leading to price increases due to improved storage options. Nadorcott was primarily delivered from Turkey, with Murcott adding to the mix. Nadorcott was also mainly unloaded from Morocco. Italy provided a few batches: Mandared size 1xx cost €20 per 6-kg package in Frankfurt and sold quickly due to their appealing organoleptic properties. The first Spanish Orri are expected to appear in week 05.

According to BLE, marketing was generally quiet. In the mandarin sector, both rising quotations and price reductions were observed. The availability of Spanish, Moroccan, and Italian batches in the clementine sector was limited. As a result, traders were able to increase their previous prices due to quantity constraints.

Apples

Domestic offers, especially Elstar, Jonagold, and Wellant, continued to dominate. The supply was sufficient to meet demand. Interest had intensified slightly in some cases. However, prices often remained at the previous week's level.

Pears

Italian, Turkish, and Dutch products formed the basis of the assortment. Unloadings from Germany, Belgium, and Spain completed the range of goods.

Grapes

Crimson Seedless have now joined the abundant South African offers. Light and blue fruits often became cheaper, while the ratings of red items frequently increased.

Oranges

Prices tended to be more downward than upward: a certain customer saturation was undeniable.

Lemons

Primofiori from Spain dominated the scene. Meyer lemons, Enterdonato, and Lama were delivered from Turkey. Eureka came from Egypt, but they could not consistently convince in terms of quality.

Bananas

Traders adequately adjusted their provisioning to the storage possibilities. As a result, prices rarely changed.

Cauliflower

In addition to the dominant Italian batches, Spanish offers were primarily available. Deliveries from France, Belgium, and the Netherlands supplemented the business.

Lettuce

Iceberg lettuce came almost exclusively from Spain. Availability had expanded. In addition, there were occasional returns from the retail trade. This then resulted in price reductions, some of which were quite significant.

Cucumbers

Spanish cucumbers dominated the scene. However, the presence of Belgian and Dutch offers was growing.

Tomatoes

The range was diverse, and the prices were accordingly varied. Customers rarely had any quality complaints. Nevertheless, prices generally tended downwards.

Vegetable peppers

The dominant Spanish offers were mainly flanked by Turkish imports. In addition, a few Moroccan deliveries could be accessed, which rounded off the range of goods in total.

Source: BLE