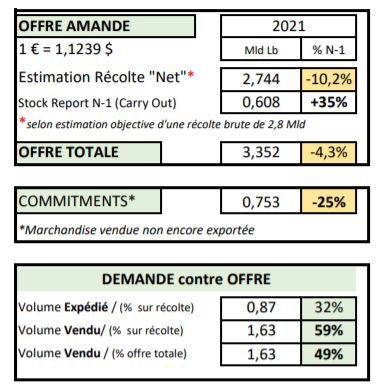

The pace at which Californian almonds from the new harvest are being received by the huskers is slowing down. The consensus for the final size still remains around 2.8 billion lbs (-10%. vs. N-1). This figure will be confirmed in January because, historically, 96% of the harvest is received by the end of December. Producers are now shifting their focus to the level of precipitation (rain/snow) because the water allocations for the coming year are still non-existent (0%). Most of the almond producing regions are indeed placed in the “rare drought” category and will not have priority for future water allocations unless the reservoirs, currently at historically low levels, get enough water this winter.

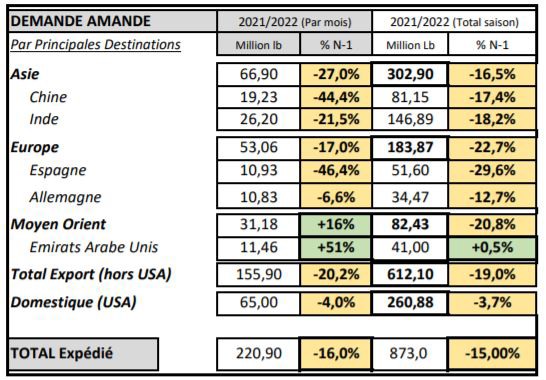

To this date, the volumes sold correspond to 48.5% of the total available offer (compared to 58% in N-1), the lowest level since 2014/2015, which was a drought year. With very few exceptions (Japan/United Arab Emirates), all the main destinations for Californian almonds are reporting a clear decline in imported volumes in November for the third consecutive month. The domestic market is less affected (-4%; less complicated logistics). Exports are truly in decline (-20%) on the traditional markets (Europe: -17%, Spain: -46%...), and on the markets that are highly sensitive to prices (India: 21%, China: -44%). This situation was expected, as the consequence of a mechanism in place for several months. A large stock was shipped during the summer resulting in fewer new sales (lack of willingness from producers to sell at production costs) and a drop in commitments, which slowed down the volumes shipped and to be shipped (also partly due to recurring logistics problems in Oakland…). But this dynamic should be interrupted because the stocks in Europe and Asia will eventually be exhausted; these strategic markets are not well covered in the long term and will therefore have to take new positions.

Stabilized prices

The interest from buyers has increased considerably in recent weeks but was confronted with the indifference from sellers who only want to offer in the long term with significant premiums. Prices stabilized around 2 USD/lb FAS for Std5. At the end of the year, growers, who retain most of the stocks, are not likely to trade until the final size is finally confirmed for the 2021 harvest.

For more information:

Louis Pimpaud

KANOPEE Sarl

28 rue Gabriel Lippmann

L-1943 Luxembourg

Phone: + 352 27 91 45 56

Cell: + 352 621 26 34 54

[email protected]

https://kanopee.lu/