Consumer behavior is globalizing, but the expression of that behavior is highly localized. That's a key takeaway from a recent presentation from the International Fresh Produce Association's annual Global Intelligence Consumer Tracking Study which gives standardized insights across seven major markets that represent 580 billion in fresh produce imports annually.

Rachel Blake, manager of global intelligence for IFPA, outlined some key insights from the survey in last week's webinar and notes that these markets represent different stages of development, different cultural contexts and different economic realities.

She noted that companies must balance global consistency with deep local relevance. While consumers around the world increasingly share the same fundamental expectations—quality, value, safety, community support, and environmental responsibility—the way they define, prioritize, and act on those expectations varies significantly by market and by generation. This means businesses cannot rely on a single global product, pricing, or messaging strategy. Instead, they must anchor their strategies in universal consumer drivers while tailoring execution to local cultural, economic, and demographic realities. Success will depend on strong market intelligence, flexible operating models, and the ability to translate shared global values into locally meaningful offerings that resonate with specific consumer segments.

Here, these five trends that rise to the top around the world.

The importance of local: This is universal across all markets, Blake notes. Between 63 and.80 percent of consumers are willing to pay premiums for local, with South Korea leading around 80 percent and the UK at the lower end around 63 percent.

However, what qualifies as local is very different by market–in Asia, local means the same country and in Europe, it's the same region. In the U.S.? Consumers are thinking about the state or county level.

Generationally, Gen. Z drives this trend everywhere, though the intensity of that generational gap varies significantly by market. In the U.S., Gen. Z comes in at 81 percent preferring local while baby boomers, 65 percent.

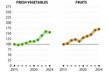

Meanwhile, U.S. imports continue to grow annually and last year, the country imported $38 billion worth of fresh produce. That's up eight percent from the previous year.

"Local" has ultimately become a powerful marketing and positioning lever rather than a strict supply-chain requirement, and companies that understand this distinction can capture premium value without limiting sourcing flexibility. While a majority of consumers across markets are willing to pay more for "local," what qualifies as local varies widely by region—from country-level in Asia, to regional in Europe, to state or county in the U.S.—and the demand is most strongly driven by Gen Z. At the same time, rising U.S. produce imports show that stated preferences for local are not translating into reduced demand for imported products.

For businesses, this means success lies in aligning origin storytelling, transparency, and community connection with local consumer definitions, while continuing to optimize global sourcing. Brands that credibly communicate proximity, connection, and purpose—without assuming consumers will materially change buying behavior—are best positioned to justify premiums and maintain scale.

© IFPA

© IFPA

Sustainability: This category sees dramatic regional differences. In China, 77 percent of consumers factor sustainability into produce purchases and the U.S. is 54 percent. Generationally, Millennials come in at 64 percent consideration versus Baby Boomers at 46 percent. That's an 18 point gap affecting everything from sourcing to marketing produce.

Across all markets, pesticides are the top sustainability factor globally, but the intensity varies dramatically by region. Country of origin and packaging type follow as secondary factors.

Blake says this creates different business realities across regions. In Asian markets it's often the older consumers driving sustainability while in Western markets, it's younger consumers. Ultimately, Blake says sustainability is becoming table stakes for market access in Asia, but it's still a premium differentiator in the West.

Sustainability requires region- and generation-specific strategies, not a single global approach. While sustainability strongly influences produce purchasing in some markets—such as China, where it is effectively a baseline expectation—it plays a more differentiated role in others, like the U.S., where it remains a premium attribute rather than a requirement. The large generational gap, particularly in Western markets where Millennials drive sustainability demand far more than Baby Boomers, means companies must align sustainability investments with the consumer segments that value them most. Globally, concerns around pesticides dominate sustainability perceptions, followed by country of origin and packaging, but the intensity of these concerns varies widely by region.

For businesses, this translates into different commercial realities: sustainability is increasingly necessary to compete at all in Asian markets, while in Western markets it can be leveraged selectively to justify premiums, strengthen brand positioning, and target younger consumers without over-investing where demand is weaker.

Price sensitivity: Australian consumers report the highest price stress of 53 percent while Chinese consumers show the lowest at 28 percent. This difference matters because Chinese consumers' lower price stress creates conditions where they're willing to pay premiums for quality imports while high stress markets resist premium positioning.

Younger consumers report higher price stress. In the U.S., Blake says Gen. Z reports the highest price stress at 73 percent, and that has risen over the last six months considerably. Yet they're driving every premium trend tracked.

These aren't small differences. These are business changing demographic realities shaping how the U.S. market operates.

Ultimately, consumers will pay more, but they need to believe they're getting more value.

Packaging: Packaging might be the most culturally divided trend tracked.

Chinese consumers seek packaging as safety and convenience with 48 percent believing that it's safer than unpackaged produce. Germans consumers, however, see it as waste–only 28 percent share that safety perception.

However universally, Gen. Z accepts packaging everywhere. In Australia, 47 percent of Gen. Z will buy packaged produce, versus 15 percent of baby boomers. In the U.S., packaging shows the most dramatic divide with 41 points between Gen Z. acceptance of packaging and Baby Boomer resistance.

© IFPA

© IFPA

This suggests that packaging acceptance is going to grow over time as populations turn over. For the industry, this means completely different product strategies may be needed by the market today, but convergence could be expected in the future.

Organics: The numbers show it is strong globally, but the real story is about age driving values, not just income driving purchasing power.

China leads with 86 percent more likely to purchase organic with Germany close behind at 79 percent. Even the lowest markets, U.S. and Brazil, still show strong organic appeal across all income levels.

What's driving this isn't just who can afford organic. It's age-based values around sustainability. Blake says age determines the likelihood of who considers organic, while income determines the ability to act on it. The sweet spot is young, higher income consumers who have built the value and the means.

The generational leadership varies dramatically by reach as well. In China, it's Gen. X leading. In Brazil, Gen X hits 81 percent, but in the U.S. it's millennials at 81 percent, and that number has risen over the last six months considerably. These generational shifts towards sustainability consciousness appeared more fundamental than pure purchasing power, driving organic demand globally. The numbers show organic demand premiums everywhere but the target and strategy needs to account for which generation leads organic adoption in each specific market.

For more information:

For more information:

Ashley Sempowski

International Fresh Produce Association

[email protected]

https://www.freshproduce.com/