According to the BLE, Spanish offers dominated the market. They played a particularly important role in Berlin, where fruit in size 32 mm+ cost around €8 per kg. In Hamburg and Cologne, their presence had expanded noticeably, which is why they were cheaper. In Frankfurt, their quality was not entirely convincing, which is why customers increasingly turned to Turkish imports. These arrived in Munich in greater numbers, which is why prices crumbled a little and were popular with buyers despite comparatively high valuations.

In Berlin, Napoleon and Sahili were largely tied to the food retail trade. Greek and Italian deliveries complemented the scene, but occasionally left something to be desired in terms of quality. Domestic batches were in short supply and slightly more expensive. Overall, availability was somewhat limited. Nevertheless, demand could generally be met. Small products were often ignored by customers, while larger items were more sought-after. Prices often fluctuated, but on the whole tended to go down rather than up.

Apples

New Zealand and Chilean Royal Gala apples now formed the basis of supply, followed by South African Braeburn and Chilean Elstar in terms of importance. Shipments from overseas had increased overall.

Pears

The low demand was easily satisfied. Prices often remained at last week's levels.

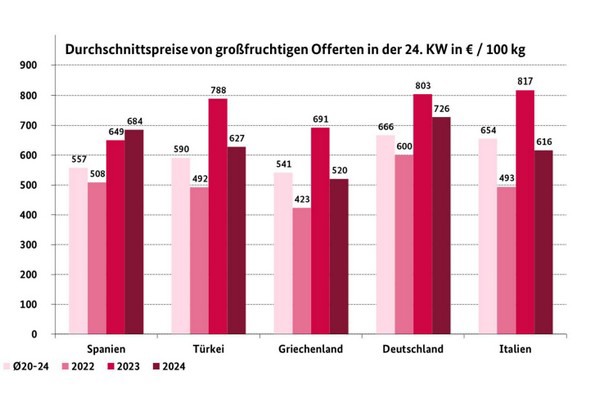

Grapes

Italian Black Magic and Victoria were at the top of the range and were flanked by Arra 30 and Flame Seedless. The first Italian Michele Palieri also arrived towards the weekend.

Strawberries

The availability of the dominant domestic lots was obviously limited. Demand was sometimes quite modest, and the quality of the leading domestic items was not always convincing.

Apricots

Spanish batches predominated over French ones. The range was supplemented by Italian and Greek batches.

Peaches/nectarines

Demand was not particularly strong and could be met without difficulty. Traders sometimes lowered their prices, which helped to speed up business a little.

Lemons

Spanish shipments predominated, South African shipments were only of a supplementary nature. Availability was sufficient to satisfy the demand.

Bananas

As a rule, the supply was sufficiently adapted to the accommodation possibilities. The traders therefore only very rarely had to modify their previous prices.

Cauliflowers

Domestic batches dominated, but had lost relevance overall. Overall, availability was limited, but demand could usually be met.

Lettuce

In the case of iceberg lettuce, German, Dutch and, to a lesser extent, Spanish offerings were available. The latter often exhibited quality problems towards the end of the season.

Cucumbers

Availability had increased slightly. Interest could not always keep pace with this. The markets reported in unison that prices had fallen.

Tomatoes

Belgian and Dutch deliveries dominated the market. Despite slightly limited availability, demand was met. Interest was very favourable.

Sweet peppers

Dutch deliveries dominated, with Turkish and Belgian deliveries completing the picture. A few domestic lots were also available.

Asparagus

The season entered the home straight: The availability of domestic offerings was drastically reduced. However, customers were still buying up large quantities. It was therefore not surprising that prices rose, in some cases quite significantly.

Source: BLE