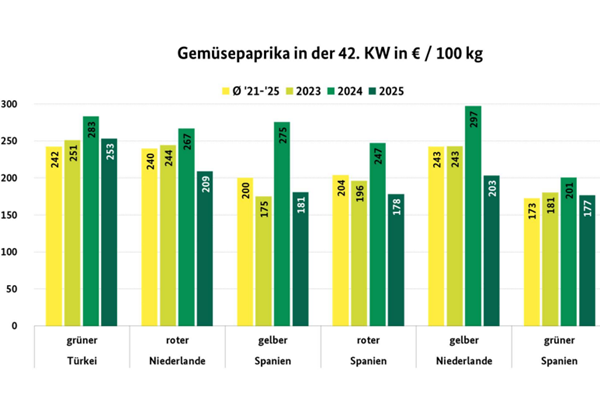

Dutch and Spanish peppers formed the basis of the supply, alongside predominantly Turkish pointed peppers. Polish and Belgian shipments complemented the scene in this segment. In Munich, customers still had access to regionally grown peppers in all three colors, while in Frankfurt, products from Franconia were fetching an impressive EUR 4 to 5.

Imports from Spain gradually increased, while Central European supplies slowly declined a bit. Even though the Spanish peppers encountered were still somewhat small locally, they were often cheaper than the competition from the Netherlands and Belgium. In addition, pointed peppers from Spain were now appearing more frequently in the markets.

In general, the gradual change in caliber and quality resulted in more differentiated loads, which led to wider price ranges. All in all, prices stabilized slightly, especially for regular yellow and red loads from all origins. Depending on the size, prices for 5 kg cartons ranged between EUR 8 and EUR 11. In Berlin, prices for Turkish products remained at EUR 15 to EUR 18 per 6 kg package.

© BLE

© BLE

Click here to go directly to the full market and price report.

Apples

Domestic products dominated the market and gained further importance. Elstar, Jonagold, Boskoop, Royal Gala, and Braeburn formed the basis of the supply. Pinova, Wellant, and Topaz, which are becoming more prominent, complement the scene. In addition, Italian, French, New Zealand, and Chilean produce were also available.

Pears

Italian Abate Fetel and Santa Maria, as well as Turkish Santa Maria, dominated the market. Green and red Williams Christ pears were available locally from Italy. Turkey now supplies more large-fruited Deveci pears. From Germany, Alexander Lucas, Williams Christ, Xenia, and Boscs Flaschenbirne/Kaiser Alexander were primarily available.

Table grapes

Italian deliveries clearly dominated the market, with Italia and Red Globe playing the most important roles. Turkey mainly supplied Sultana and, to a lesser extent, Crimson Seedless. Supplies from Moldova, Greece, and France supplemented the market.

Small citrus fruits

The satsuma season from Spain is already in full swing. Okitsu and mostly green-skinned Iwasaki and Miyagawa, often with leaves, dominated the market. Mandarins from South Africa and Peru were still available in abundant quantities and sold well with Tango, Nadorcott, and a few Orri.

Lemons

South African loads continued to dominate in terms of volume. Spain followed, with Argentina and Chile supplementing locally on a smaller scale. Overall, the presence of Spanish loads expanded noticeably with the Primofiori and Verdelli varieties.

Bananas

Due to the autumnal weather, retailers recorded stable sales and virtually unchanged selling prices. Locally, there were minimal price reductions for various origins and brands. In Frankfurt, Del Monte had to make price concessions daily due to advanced ripeness.

Cauliflower

The supply was based on domestic, Belgian, and, in Berlin, Polish supplies. The Netherlands and France also contributed some quantities to the stores. Overall, availability was slightly limited. The autumnal weather had improved storage conditions in some areas.

Lettuce

Domestic and Belgian lettuce was available. Dutch products dominated the iceberg lettuce segment ahead of domestic products, and supplies from Spain appeared to increase. Mixed lettuce was exclusively sourced domestically.

Cucumbers

Supplies of Spanish cucumbers slowly intensified but still lagged behind Dutch and Belgian loads in terms of volume. Domestic supplies also declined in volume and complemented the market scene.

Tomatoes

The supply continued to be dominated by Belgian and Dutch vine, round, and cherry varieties. Italian cherry varieties, Turkish vine tomatoes, and Polish beef and round tomatoes completed the assortment. Various German products continued to be represented on the markets to a lesser extent.

Source: BLE