As Rabobank is one of the most well-known financial institutions in the agricultural industry, growers might often turn to it for funding their facilities. Lambert van Horen, however, explained there's a difference between investing and financing. "An investor, who's active in equity, takes some risks and wants a nice profit for this risk-taking behavior. In finance, it's more about minimizing risks, ensuring small margins for the bank," he explained during his keynote at the Leafy Hydroponics Summit.

Rabobank is a cooperative institution focusing on food and agriculture. Lambert explained to the 200+ attendees that Rabobank works not just with growers, but also with suppliers, propagators, wholesalers, and others in the chain. When it comes to financing a project, it all starts with the client, he says. "First, we assess the client's needs. Next, we explore possible solutions (lease, asset financing, lowest cost options) and under what conditions a client can be helped. Sometimes, we can't, or won't, provide financing," he explained.

Purpose

Looking at the horticultural industry, it's clear there's no one-size-fits-all recipe for success. Only looking at the definitions and systems in the industry, there's a lot of diversity and a lot of confusion. In North America, various indoor farming solutions—whether it's a rooftop greenhouse, plant factory, or aquaponic facility—are often grouped under CEA (Controlled Environment Agriculture), despite significant differences. Also, the goal of a facility is important to specify. "Five years ago, there was much confusion about projects with social goals. A social goal is fine, but it's different from a commercial business. Definitions are key; discuss your plans with your financier. It's crucial to help a banker understand your business plan and the purpose of the investment."

And even if your goal is clear, there's no one ideal solution, as the local situation varies everywhere. "Climate, market conditions, water availability, and regulations," Lambert says. However, globally, systems are becoming more capital-intensive. "We see the evolution from simple open field solutions to hail nets or plastic covers to mitigate risks, mid-tech solutions like multispan facilities, and greenhouses with higher capital expenditure and often higher operational expenses, and finally to daylight-free cultivation systems." Combining different systems may also be an option, depending on market demands.

Banking principle

So what's the role of Rabobank? Lambert explains that, in general, banks have a moderate appetite for risks. "We work with savings from the other part of the balance sheet and focus on relatively low return on investment periods, low risk, and flexible facilities. This can contrast with investors who seek high-risk and higher returns." However, Rabobank is a commercial company, so balancing commercial relevance with risk assessment is vital. This is also why relationship managers, meaning a grower's contact, within the bank will discuss this balance with risk managers. "Providing your bank relationship proper insights on your facility is essential, as they will be your advocate in these discussions."

Appetite for risks

How do hydroponics fit into risk avoidance? Do they offer flexibility or volatility? "Sometimes growers build greenhouses for specific crops. A greenhouse for cucumbers may look different from one for sweet peppers. Or are you building a multipurpose greenhouse for various crops?" When asked about balancing efficiency and flexibility, Lambert explained the bank does not draw this line. "The market does. If you're in an isolated place, you focus on leafy greens and only produce basil, without the ability to switch, you might need to think of your flexibility, as consumer preferences could change. Market research is crucial."

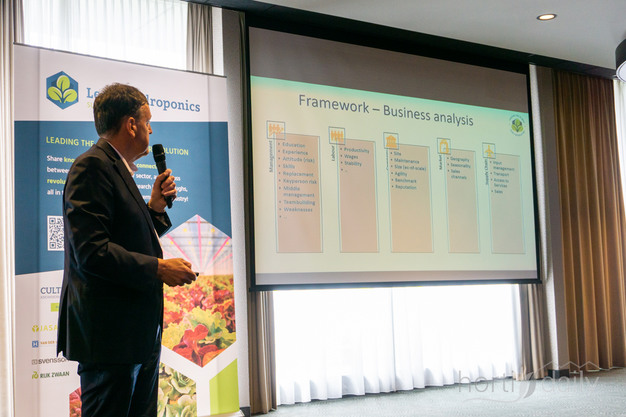

Lambert explains a solid risk assessment is foundational in getting bank support. Risk assessments involve business, financial, structural, and sustainability analyses, reflecting the bank's increasing focus on sustainability from society and European partners.

A business analysis includes labor plans (workers and management) and market developments. In this, Rabobank examines the value chain, not just the company itself. "What's the stability of your supply chain? Who do you sell to? To supermarkets? Directly, or through intermediaries? What's the value of your contract with a wholesaler if they lack a contract with a supermarket?" Relationships with suppliers are equally crucial, ensuring a stable chain and consistent production. Assessing these relationships helps understand supply chain risks, aiming for stability.

The financial analysis includes liquidity, cash flow, and profitability. When asked if Rabobank finances vertical farms, Lambert noted they still don't because the business models often lack positive cash flow. "Without positive cash flow, there's no cash to repay the loan. You can have a temporary grace period, but vertical farming companies usually reinvest all available cash, increasing risk, which requires investors, not financiers. Without risk tolerance, positive cash flow is necessary." Solvency is less relevant than other financial metrics for the bank. "We're in it for the long term; we're not interested in partnering just for sales." Rabobank has, however, invested in companies using vertical farming techniques for propagation, contributing to the overall growth chain and cycle.

Incorporate sustainability in planning

In addition to structural analysis, Rabobank also evaluates sustainability, focusing on ecological and social aspects. This includes discussions on climate change impacts on businesses and hydroponic growing. This year, Dutch greenhouses must provide an energy plan, outlining how they will be climate-neutral by 2040. "Every grower should achieve this by 2040, according to European legislation. Whether through solar panels, residual heat, or other solutions, there are numerous options, but we want to discuss with our customers how they will achieve this." He anticipates this requirement will extend to other countries soon.

Evaluate and improve sustainability

Lambert notes the bank starts with calculating footprints. "Not for comparison yet, but to raise awareness of where companies can quickly improve. Adjusting packaging, lighting installations, or biological crop protection can improve your footprint, providing valuable insights." He also mentions that new regulations pose risks for chemical crop protection usage. "We strive for ongoing dialogue with our customers on these developments."

To maintain this dialogue broadly, Lambert offers visitors some considerations, starting with market evaluation. "If you build a facility with high capex, ensure the market is stable or growing. You want it to last for 10-15 years, aligning with typical depreciation periods. Those from the greenhouse sector know they build for 20 years, requiring long-term development and market prediction. High capex facilities need long-term financing, different from outdoor facilities with a 3-5 year depreciation period."

Second, recognize that expensive facilities often lack flexibility. "If you have a range of investments and financing, you may need more investments, which is evident from our risk perspective."

Finally, consider innovativeness. "Innovations bring high opportunities and risks. While we aim to be optimistic, innovation also entails risks—some will succeed spectacularly, while others may fade within years. It's essential to consider these factors."

For more information:

Rabobank

www.rabobank.nl