As the conflict in the Middle East continues, South Africa's farming sector is monitoring rising input costs, particularly fertiliser and fuel. Current concerns are linked less to supply constraints and more to uncertainty about future price developments, while questions remain about potential effects on consumer food prices.

There is no immediate fertiliser shortage, but prices are increasing due to concerns about global supply disruptions and the role of the Middle East in fertiliser inputs. The duration of the conflict will determine the extent of market pressure. The next major fertiliser usage period begins in October with summer crop planting. If logistics conditions in the Middle East improve before June, price pressure may ease ahead of the 2026-27 production season.

Fertiliser costs remain a key factor for producers. Fertiliser accounts for 35 per cent of grain farmers' input costs and a substantial share for other crops. South Africa imports roughly 80 per cent of its annual fertiliser requirements. Farmers are price-takers and cannot pass these costs directly to consumers. In some cases, planting decisions may be adjusted, but this is not expected in the near term.

Fuel prices are also under observation. Supply remains generally stable, although demand ahead of April price adjustments could create localized disruptions. Fuel is a cost component across value chains, with peak use during planting and harvesting periods. Winter crop planting in the Western Cape starts at the end of April, followed by other regions, while grain harvesting begins in May and citrus harvests follow. These periods are associated with higher fuel use.

Despite cost pressures, general supply conditions across most regions remain stable. This places pressure on margins rather than availability.

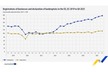

Consumer food price inflation is expected to moderate in 2026, supported by ample domestic supplies of grains, oilseeds, fruit, and vegetables. Data from Statistics South Africa show food price inflation slowed to 3.7% in February 2026, down from 4% in January. However, fuel prices remain a risk factor due to their role in distribution costs. Around 80 per cent of grain and a large share of other products are transported by road, allowing fuel price increases to be partially passed on to consumers.

There is typically a lag between input cost increases and retail food prices. Current supply levels following a favorable agricultural season are expected to limit short-term price movements.

Source: Wandile Sihlobo