The European potato market is under pressure due to a significant surplus, in some cases forcing growers to pay to market their product, reports DCA Market Intelligence. The large supply has led to weak demand, and low prices or even free distribution are not sufficient to reduce stocks.

Dutch arable farmers and their counterparts in Belgium, Germany, and France have significantly expanded their potato acreage over the past two years, driven by strong demand and favorable contract prices from the processing industry. Favorable growing conditions resulted in high yields in 2025 and consequently a large harvest.

However, demand for potatoes has clearly weakened. Increasing competition from Asia, import duties in the United States, and a weaker dollar have put pressure on the export position of European producers. This has created a structural surplus.

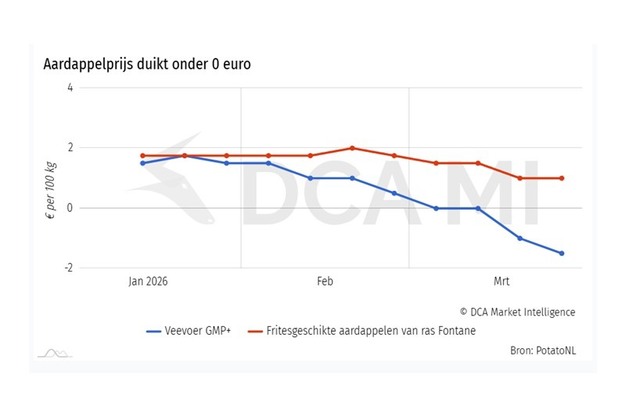

Pricing reflects this situation. PotatoNL recently quoted €-1.00 to €-2.00 per 100 kilos for feed potatoes, while prices for processing potatoes are only slightly higher. The surplus is shifting volumes toward animal feed and biofermentation, with marketing costs increasingly falling on growers, partly due to higher transport costs.

© DCA

© DCA

Time pressure ahead of the new harvest

Although potatoes can technically be stored for a long time, their economic viability is declining. With no prospect of price recovery, growers are choosing to reduce storage costs and sell earlier. "Not everyone can store their potatoes for that long. Moreover, there is currently no prospect of market improvement. So growers are deciding to stop incurring costs to refrigerate potatoes," said Niels van der Boom, potato market specialist at DCA Market Intelligence. As a result, additional volumes are entering the market more quickly, while storage space is needed for the new crop.

Surpluses in the Netherlands and surrounding countries are substantial. The Netherlands harvested around 4.2 million tonnes of consumption potatoes in 2025, 900,000 tonnes more than a year earlier. Some of this volume has already been diverted to feed, fermentation, or starch processing, but an estimated 500,000 to 600,000 tonnes still remain.

Other countries are also facing large surpluses. In Belgium, around 800,000 tonnes are in storage without a buyer, in France, the surplus is estimated at 1 million tonnes, and a similar volume is expected in Germany. Based on DCA Market Intelligence estimates (2025), this brings the total surplus in the EU-4 to around 3.3 million tonnes.

Promotional campaigns

In Belgium, promotional campaigns are being launched to market potatoes for food, feed, or as a raw material for biogas. In France, GIPT and Arvalis are working on a protocol for controlled destruction to reduce health risks.

In the Netherlands, the issue has been discussed, but concrete measures have so far not materialized. Given the scale of the surpluses, broader initiatives are needed to create sufficient space ahead of the new harvest.

The current situation highlights the need for market players to adjust production, contracting, and marketing strategies in line with structurally changing market dynamics.

Source: DCA Market Intelligence