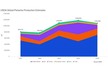

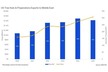

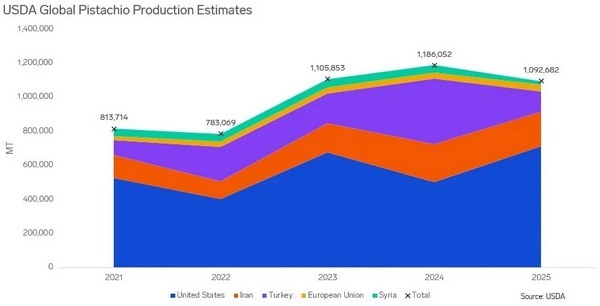

The United States, Turkey, and Iran remain the three largest pistachio producers and exporters, accounting for most global supply. Market sources indicate that the 2025 harvest produced about 712k MT in the United States, around 135k MT in Turkey, and roughly 225k MT in Iran, all on an inshell basis. Combined, these origins represent the majority of global production, with industry estimates placing total 2025 output at 1.1 to 1.2 million MT of in-shell pistachios.

Pistachio production follows a two-year cyclical bearing pattern. In 2025, the United States and Iran were in on years with stronger production potential, while Turkey was in an off year. In 2026, the cycle is expected to rotate, with Turkey moving into an on-year and the United States and Iran entering off-year positions. Iran's production generally shows less pronounced swings than the United States and Turkey, although variability still occurs.

© USDA

© USDA

Iranian pistachio exports were already facing disruption before the recent military escalation in the region. Since at least January 2026, exporters have encountered constraints linked to internal unrest and government crackdowns that included internet and communications shutdowns. These conditions limited interaction with international buyers and have already affected export activity. The military escalation is adding pressure to an already restricted situation.

The 2025 Iranian crop was smaller than expected, with drought and dry weather widely cited by market participants as the main reason. The 2026 crop remains at an early stage of development.

Within Iran, pistachio orchards are concentrated mainly in northeastern regions, although production is also present in other areas. According to recent reports, military activity has been less extensive in eastern regions compared with western and southern parts of the country. At this stage, it remains unclear whether orchards have experienced direct damage.

Market participants indicate that near term impacts are expected to be primarily logistical. Concerns focus on how much product will reach international markets if the conflict continues. Even buyers who do not normally source from Iran may face increased competition for supply from other origins.

Direct trade with Iran has long been limited by sanctions. Historically, volumes have moved through trading hubs such as the United Arab Emirates and Turkey before reaching international markets. These hubs also handle other tree nuts and a wide range of goods. Shipping disruptions in the region are expected to affect these transit points and may influence trade flows to the Indian subcontinent and the eastern Mediterranean.

Buyers may increasingly rely on U.S. supply, although U.S. sellers are reported to be well committed and cautious with new sales as the next U.S. crop enters an off-year. Turkey is also facing limitations due to its smaller 2025 harvest and shipping disruptions affecting routes through the Red Sea and Suez Canal.

Market participants indicate that supply disruptions are likely to support steady to firm pricing conditions, given the tighter availability across major producing regions.

Source: Mintec/Expana