EU producers of frozen fries continue to face reduced demand from non-EU markets, despite lower export prices, while overseas suppliers increase volumes. Competition from China and India has intensified, prompting European producers to adjust pricing.

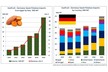

The average export price of frozen fries in November 2025, based on the latest available data, stood at €1,154 per metric ton, equivalent to about US$1,260 per metric ton. This represents a year-on-year decline of 11.8 per cent and marks the lowest level recorded since November 2022.

Export performance varied by destination. South America recorded an 8 per cent increase in EU frozen fry imports in the year to November 2025 on a year-on-year basis. In contrast, volumes shipped to the UK and the Middle East declined by 9.6 per cent and 19.4 per cent, respectively, over the same period. Australasia, which represents a smaller share of EU exports, saw volumes fall by 34.5 per cent.

Among the EU-5 exporting countries, Belgium, the Netherlands, France, Germany, and Poland, which together account for more than 90 per cent of EU frozen fry exports, shipments to non-EU markets were down by 7.9 per cent in the year ending October 2025. Total exports from these countries declined by 2 per cent over the same period.

Saudi Arabia remains an important destination for EU fries, although competition has increased. Between November 2024 and October 2025, Indian frozen fry exports to Saudi Arabia rose by 312 per cent year on year. In volume terms, Indian shipments reached about 15 per cent of the combined contribution from the Netherlands, Belgium, and France, compared with 3.6 per cent one year earlier.

Market sources indicate that lower volumes shipped to the UK may be linked to weaker foodservice demand, where most imported frozen fries are used, as well as high domestic supply levels.

Sources told Expana that EU processors may need to maintain price pressure in order to retain positions in key overseas markets, particularly in the Middle East. Reduced export demand is occurring alongside oversupply in the current European potato season. In addition, processors entered the 2025/26 season with a high level of contracted raw material, resulting in limited free-buy trade availability.

Source: Mintec/Expana