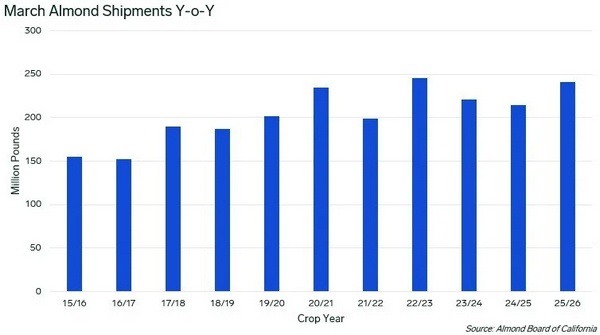

The Almond Board of California reported March shipments of 258.0 million pounds (117,028 tons) for the 2025/26 season, up 16.5% year-on-year and above market expectations of 228 million pounds. Industry sources linked the result to continued shipment momentum, with Europe contributing through stock replenishment, while Middle East volumes remained stable with trade flows shifting toward Türkiye.

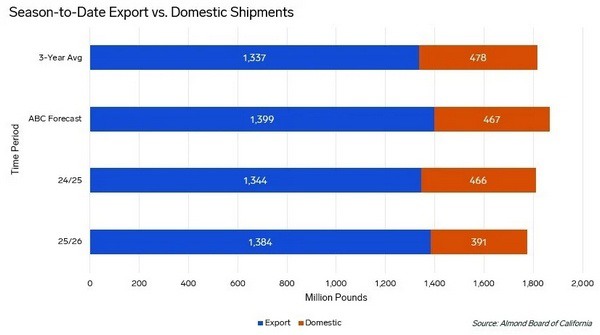

Season-to-date shipments from August to March reached 1,775.8 million pounds, down 1.9% year-on-year, improving from a 4.4% deficit in February. March shipments included 52.8 million pounds domestically, up 1.9%, and 205.2 million pounds exported, up 21.0%. Export share stands at 78%, above the Almond Board of California forecast of 75% and the three-year average of 73%. Domestic shipments remain down 15.9% on a season-to-date basis.

© Almond Board of California

© Almond Board of California

Key markets included India at 39.2 million pounds for March, with 252.3 million pounds season-to-date, down 3%. Europe received 77.3 million pounds in March, bringing the total to 461.3 million pounds, up 7%. The Middle East recorded 21.9 million pounds for the month and 255.0 million pounds season-to-date, up 4%, although shipments reflect rerouting activity. China and Hong Kong totaled 4.1 million pounds in March and 24.3 million pounds season-to-date, down 45%, with some renewed inquiries linked to supply issues in Australia.

Total commitments reached 576.1 million pounds, up 0.4% year-on-year. New sales for March totaled 240.7 million pounds, up 10.6% from the previous year, while slightly below February's 246.2 million pounds.

Crop receipts reached 2,684.4 million pounds through March, down 0.6%, with March receipts at 4.9 million pounds. The industry continues to work with an estimated crop size of 2.7 billion pounds, with sold positions at 75.1% of supply.

© Almond Board of California

© Almond Board of California

Market participants reported price adjustments in Europe following the report. Some indicated improved sentiment linked to shipment performance and sales activity, while noting ongoing uncertainty in demand, particularly in domestic and Middle East markets. Buyers continue to focus on short-term coverage.

Upcoming data releases, including the Land IQ acreage estimate and the USDA subjective estimate, are expected to provide further direction for the 2026 crop outlook.

Source: Mintec/Expana