Belgium

Fiwap/PCA market message:

The atmosphere remains somewhat gloomy despite the weather which has kept the rates steady and looking valuable. There are delays in fast planting in all major production areas (West Flanders, Palatinate , Lower Saxony and Rhineland), and German trading continues to deliver potatoes (mainly Fontane) contracted to the Belgian industry at the time, caused by the panic of several Belgian processors facing the drought of June 2017. Export’s are difficult, with small volumes to North Africa and the Balkans. There’s tough competition from French exporters with lower prices, and better skin qualities.

Industrial varieties: general price, 35 mm +, min 60% 50 mm +, min 360 gr / 5kg of EPS, bulk, friable, selling price, excluding VAT, direct delivery:

Bintje : calm market (supply greater than, or equal to, demand). 2.00 to 3.00 €/a, depending to quality and destination; very little demand for the industry; on the other hand, peelers remain buyers of the best batches (size and roast);

Challenger : stable market (supply equal to demand). Price around € 3.00/a. Buyers remain attentive to internal defects with strict tolerance applied;

Fontane : market much stronger (demand greater than supply) with price at € 5.00/a. Increasing demand for immediate delivery AND for delayed delivery (at higher prices). The market, more or less blocked, could unlock once better rates are available.

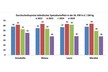

European physical markets

Summary of rates (source: NEPG):

Bintje plant/other varieties "fries": low supply of small sizes, and rising prices. Overall demand delays due to bad weather, which postponed the planting period. Dutch plant, class A, made in April 2018, per 5 tons, in bags, excl. VAT:

Size 28 - 35 mm : 60,00 – 64,00 €/q

Size 35 – 45 mm : 30,00 – 32,00 €/q

Future market

EEX in Leipzig (€/a) Bintje, Agria and various related for conversion, 40 mm+, min 60 % 50 mm +:

Netherlands

The main PotatoNL rating (fries cat 1, NeBeDe) last Thursday was valued, as were those of Innovator & Cie, and Fontane. Good trade to the south of Europe as well as to the Balkans. Producer prices for export are between 4.00 and 6.00 €/a, depending on variety and quality. For the domestic fresh markets: 8,00 to 12,00 €/a in varieties with soft pulp, 8,00 to 13,00 €/a in firm pulp (in boxes and fridge for the latter).

Cotation PotatoNL : also available on www.potatonl.com

VTA quotation (Verenigde Telers Akkerbouw)

Quotes all up, compared to those of past week:

France

For the industry, demand is better, with optimistic prices: Fontane around € 4.00/a (+ € 1), Markies around € 5.00/a (+ € 2), Inno at 5.00 €/a (+0.5 €), while Bintje remains capped at € 2.00/a . The storage quality problems continue.

On the fresh market, exports continue to Spain (Monalisa and fries between 9 and 11.00 €/a), the FRG (soft pulp between 12 and 14.00 €/a), Italy and Eastern Europe (Agata, around 13.00 €/a), etc. (source: UNPT)

Unwashed industrial potato, bulk, selling price, excl. VAT, North Seine, €/a, min – max (avg) (RNM):

Market more firm, especially on the free Fontane. Awards supported in Innovator among others.

State of stocks (source UNPT/CNIPT)

As of February 1st, 1,939,000 tons remain in stock, which is 359,000 tons (or 22.7%) more than on February 1st, 2017. 57.7% of this stock is intended for the industry (of which 79.4% committed (to contracts, sales)) and 42.3% for the fresh market (26.2% committed)

Germany

On the fresh market, producer prices remain unchanged. On April 3rd, prices had been estimated at 11.83 €/a for firm pulp, and 11.08 €/a for soft pulp. On March 27, they were unchanged at 11.67 €/a (=) for firm pulp, and at 11.00 €/q (=) for mainly firm pulp/mealy (= soft pulp). The hope of a more dynamic trade before the Easter holidays has not really manifested. In potatoes for the industry (fries), markets in Rhineland (and elsewhere in Germany) for Fontane and Challenger on one hand, and Innovator and Agria on the other, are much stronger, with producer prices between € 4.00 and € 4.50/a for Font./Chal. and between 5.00 and 5.50 €/a for Inno / Agria. Chips/crisps, unchanged but firm prices, especially in the east of the country.

In organic potatoes, producer prices are always around 48,00 €/a.

Great Britain

Average producer prices (all markets combined) by the end of week 13: €12.08 (£ 10.56), up 14.9%. The high quality Maris Piper is particularly sought after, which explains the rather serious rise.

Early plantings are severely disrupted throughout the UK, including in the Channel Islands, Cornwall and Scotland.