The citrus adviser of Uruguayan Ministry of Agriculture and Livestock, Federico Montes, analysed the sector and made predictions for the future.

What's the situation like in the citrus sector?

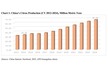

Today, barely 30% of the production is exported, which is only slightly more than in 2012, when frosts cause damage in many citrus production areas. In 2015, exports will amount to 98,000 tonnes, compared to 130,000 tonnes two years ago. Why? Firstly, because there were health issues caused by the rainy spring and summer, which affected the fruit, thus preventing growth in the European Union (EU) and Brazil; and secondly, because South African fruit, our main rival, was more competitive in the Russian market, which is a traditional destination for Valencia oranges. South Africa had a greater yield per hectare, higher productivity and lower costs. We are out of the market with the Valencia, and the Valencia accounts for 40% of our productive area and exports. We've had to switch our focus to the production of mandarins.

Were you surprised by this?

No. In 2010, when we developed the Strategic Plan for the citrus industry, we faced the dilemma: do we work on the commodity (oranges) or a specialty (mandarins)? And the sector decided to go for the specialty, because it has more value added. Not everyone can do it, because the fruit requires very good colour, flavour, a good sugar level and a balance of this with acidity. Orange is sold in bulk, mandarins have to be selected. Uruguay is competitive in the production of mandarins (better than Chile and Peru, which are its competitors), but not oranges.

Is it a crossroads towards a productive reconversion?

Yes, clearly. The production volume of mandarins increased by 25% compared to previous years and we are at the highest level in 20 years. The citrus sector is responding to the market.

Did the opening of the U.S. market have an impact?

There were other signs from the markets, but the U.S. gave the final push to convert. Mandarins reach better prices and are in high demand, also in Europe. It has been two years with Uruguay unable to sell between 20,000 and 30,000 tonnes of Valencia oranges.

It looks like a structural problem.

Old plantations and the cultivation of old varieties, with low or no profitability and not demanded by the markets, were identified as structural problems. The Strategic Plan is mostly aimed at tackling these issues. We have defined a strategy, which, among other things, entails the conversion of plots with support from a strong public policy: the National Program for the Sanitation and Certification of citrus plants, which is managed by the Ministry of Livestock, Agriculture and Fisheries (MGAP) in partnership with the National Seed Institute (Inase) and the National Agricultural Research Institute (INIA). The volume of material given is the equivalent of 2.5 million plants. I would say our current situation is bad, because it was not a good year, but we are on a good track. Uruguayan citrus knows where it is going; it is moving in the right direction. It is a relaunch, with genetics and health.

Are there other important structural problems?

Irrigation remains a structural problem because there is no competitive rainfed citrus cultivation. We have made small progress: in 2010, 49% of the citrus area had irrigation; now, it is 54%, although 75% of the area devoted to exports is irrigated. Another issue is the need to diversify our markets. Before the opening of the U.S. in 2013, 74% of the shipments went to the EU; Russia accounted for 8% and Brazil for another 3%. While the U.S. remains the strong point in our diversification strategy, we must also continue looking for markets that pay higher prices or have lower tariffs than the EU.

What are the challenges for 2016?

Firstly, we need a more aggressive attitude at international promotion, given how tough it is to wait a long time for the opening of new markets. We must strengthen that agenda.

Secondly, we need to organise and speed up the varietal conversion within the sector's capacity, because under the current circumstances the citrus industry may be compromised. We must achieve a greater productivity per hectare and obtain higher prices.

Another tough challenge is the reconstruction of the productive matrix of small and medium producers, incorporating them into value chains. The citrus production chain must be formed by producers, entrepreneurs, breeders, receivers (of fruit), consumers, associative models and strategic alliances between them. That is a challenge that cannot be overcome in just a couple of days. You have to coordinate producers and markets with partnerships and alliances.

The final challenge is for this development in production and in the market to involve also progress in social terms, with the creation of 15,000 jobs in the framework of social dialogue. Uruguay is preparing to receive new foreign investments and there are good prospects for the sector.

Source: elobservador.com.uy