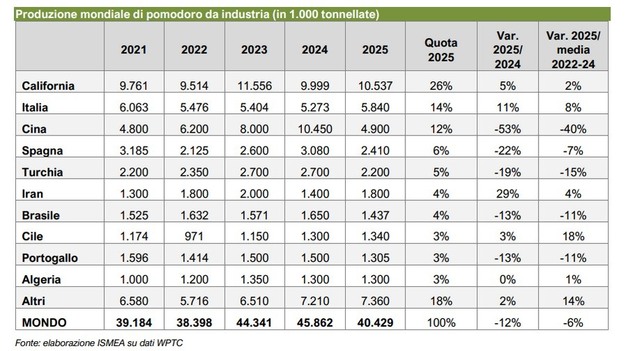

The World Processed Tomato Council (WPTC) estimates a world production of processing tomatoes of about 40.4 million tonnes in 2025 (-12% compared to the previous marketing year), mainly due to the sharp drop in Chinese production (-53%). On the contrary, Italian production in 2025 exceeded 5.8 million tonnes, i.e., an increase compared to both 2024 (+11%) and to the average of the last three marketing years (+8%). With this result, Italy returns to second place in the world ranking, immediately after the United States, followed by China and Spain, and with Turkey in fifth place. California, Italy, and China are confirmed as the main production areas, together accounting for more than half of global production.

This result confirms the weight of the national supply chain in one of the symbolic sectors of the Italian food industry.

© elaborazione ISMEA su dati WPTC

© elaborazione ISMEA su dati WPTC

Production in Italy

According to the Ismea Trends - Focus on tomato preserves report, the increase in production is due solely to the increase in surface areas: 78,700 hectares, up 3.7% compared to 2024 and 13% compared to the average of the previous three years. The campaign was instead characterised by particularly low yields: the national average stood at 74.2 tonnes per hectare, one of the lowest values of the last decade, penalised by the water crisis in Southern Italy and abnormal weather conditions in the North.

In the Northern Italian basin, cultivated areas reached 45,030 hectares, up 8% compared to 2024, driven by strong demand from the canning industry. The harvested and processed production amounted to 3,121,617 tonnes, an increase of 30% compared to 2024 and 16% compared to the average for the three-year period 2022-2024. The average yield per cultivated hectare was 69.3 tonnes, higher than in 2024 (57.8 t/ha) but lower than the historical average of the last ten years (71.0 t/ha). Yields were negatively affected mainly by the weather.

© OI Pomodoro da Industria Nord Italia

© OI Pomodoro da Industria Nord Italia

In the Centre-South basin, the number of hectares invested was 33,665, a slight decrease compared to 2024, but a 10% increase compared to the three-year period 2022-2024. In 2025, the production harvested and delivered to the processing industry amounted to 2,718,369 tonnes, a 5% decrease compared to 2024 but a 1.1% increase compared to the average of the last three years. Average yields stood at 80.7 tonnes per hectare, down about 4% from the previous year and about 7% from the average of the last decade (86.7 t/ha). The area was strongly affected by the water crisis, particularly the Foggia basin, where water shortages led to a reduction in production of about 5% compared to 2024. Product quality was good.

Foreign trade and domestic purchases

The data from the International Trade Center (ITC) also certify Italy's supremacy among the countries exporting tomato preserves for the 2024/25 campaign. In particular, Italy is ahead of China, Spain, and the USA in this ranking. Tomato preserves represent the fruit and vegetable segment with the best trade balance in Italy, a supremacy confirmed by the trend of foreign trade indicators. In the last campaign, from September 2024 to August 2025, the balance exceeded 2.5 billion euros, thanks to exports of around 4.7 million tonnes expressed in equivalent weight of fresh tomatoes (coefficient quantity) and a value of more than 2.8 billion euros.

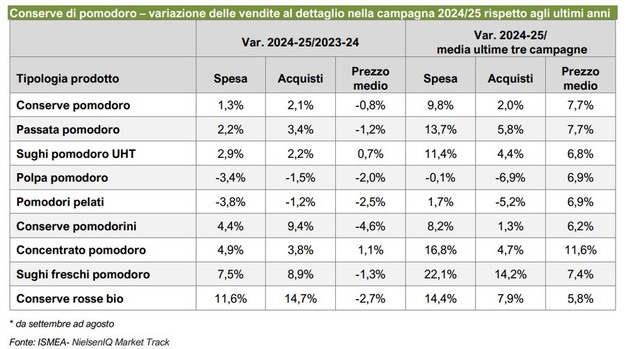

© ISMEA- NielsenIQ Market Track

© ISMEA- NielsenIQ Market Track

On the domestic market, Italian households also confirmed the central role of tomato preserves, with domestic purchases growing in the 2024/25 marketing season. Retail purchases grew by 2% in volume, an increase compared to both the previous year and the average of the last three years, reflecting a progressively expanding demand. There was also a slight reduction in average retail prices in 2025, which interrupted the price increases that began in 2022, coinciding with the surge in energy prices. The opposite dynamic between purchase growth and falling prices led to a 1.3% increase in household spending in 2025.

In 2025, the positive dynamics of the higher value-added segments also strengthened: ready-made sauces, purees, and organic preserves increased their market share, highlighting a consumer orientation towards more practical, qualified, and high service content products.

For more information:

www.ismeamercati.it