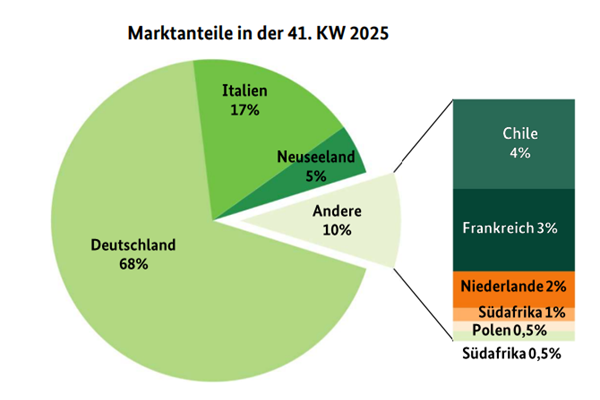

The apple assortment continued to diversify, and deliveries gained momentum once again. Domestic offerings dominated, with Elstar, Boskoop, and Jonagold leading the way. The presence of Braeburn and Rubinette strengthened once again, and the importance of Pinova and Gala also expanded.

Golden Delicious and Royal Gala were the main varieties from Italy. Deliveries from France, the Netherlands, and Poland supplemented the European supply but did not play a decisive role. The first French Jazz apples enriched the product range in various locations.

© BLE

© BLE

The autumnal weather ensured a healthy demand. However, due to the increased availability, retailers were unable to avoid discounts across the board. Imports from overseas lost relevance: Chilean, New Zealand, and South African loads left nothing to be desired in terms of quality, but their turnover was sometimes rather slow due to increased European competition.

Click here to go directly to the full market and price report.

Pears

Supplies intensified: the range consisted primarily of Italian, Dutch, Turkish, and domestic loads. Among Italian deliveries, the presence of Abate Fetel and Williams Christ increased slightly. Turkish Deveci gained market share and flanked Santa Maria from the same origin.

Table grapes

Italian products clearly dominated the market. In addition to Italia, Red Globe, and Michele Palieri, Crimson Seedless and various Arra and IFG varieties were also widely available. Turkish Sultana grapes were flanked by Crimson Seedless.

Lemons

South African fruit dominated the market, followed by Spanish fruit in terms of importance. Imports from Argentina, Chile, and Uruguay completed the product range. Although Spanish deliveries expanded, they ultimately played a minor role.

Bananas

Supply and demand were sufficiently in harmony. Traders, therefore, rarely had reason to modify their previous demands. Only in Frankfurt did customers have to dig a little deeper into their pockets for third-party brands on Friday.

Cauliflower

Domestic offers predominated, but their quality was not consistently convincing, resulting in a price gap in some cases. In Hamburg, the availability of domestic loads was too limited, so Belgian loads had to be used more frequently.

Lettuce

Domestic iceberg lettuce left something to be desired in terms of quality in some places, which is why it was delisted in some cases. Dutch and Spanish loads were more appealing in terms of quality; the latter are now also being sold in packs of 10 in Frankfurt.

Cucumbers

While the presence of Spanish batches expanded, the previously dominant domestic loads lost importance. The relevance of Dutch and Belgian products also declined as the Central European season entered its final stages.

Tomatoes

Dutch and Belgian supplies continued to dominate. Moroccan imports increased in the cherry tomato segment. Italy was primarily involved in the market with cherry tomatoes. Polish, Turkish, Croatian, and Spanish loads complemented the scene.

Bell peppers

The season for Dutch and Belgian loads was coming to an end. Availability was limited. In contrast, the Spanish campaign gained momentum: in some places, the loads already played a significant role. The increased supply led to discounts across the entire range in some cases.

Source: BLE