Reefer container freight rates continue to outperform the dry cargo trade, despite an unprecedented contraction in reefer seaborne trade last year, and this divergence is forecast to continue over the next few years, according to Drewry's recently published Reefer Shipping Annual Review and Forecast report.

The normalization of the reefer trade and resultant freight rate correction has proved more gradual than for wider container shipping, and reefer cargo demand has been steadily recovering since the start of the year, demonstrating the resilience of the trade.

Drewry estimates that total worldwide seaborne reefer cargo declined to 137.5 million tonnes last year, representing a fall of almost 1%, the first time in over 20 years and compared to flatlining trade for dry cargo. Supply chain disruptions, rising input costs, and normalization in perishables cargo demand after the peaks of 2021 all contributed to the decline. Key reefer commodities such as meat, bananas, and fresh vegetables all took a hit in 2022 as a result.

Containerized reefer trade contracted 0.7% in 2022, as the continued decline in specialized reefer ship carryings cushioned the blow of weaker cargo demand and broadly matched the fall in overall containerized liftings in the year.

Despite such adversity, reefer shipping trade is recovering through 2023, supported by steady demand from a growing world population and the recovery of Asian economies, particularly the reopening of China. These positive developments have driven a return to year-on-year growth on every key reefer-intensive trade route so far this year, with seaborne volumes projected to rise 1.5% by the end of the year. However, containerized reefer trade is forecast to expand at 2.3%, fast outpacing flatlining wider container shipping cargo demand.

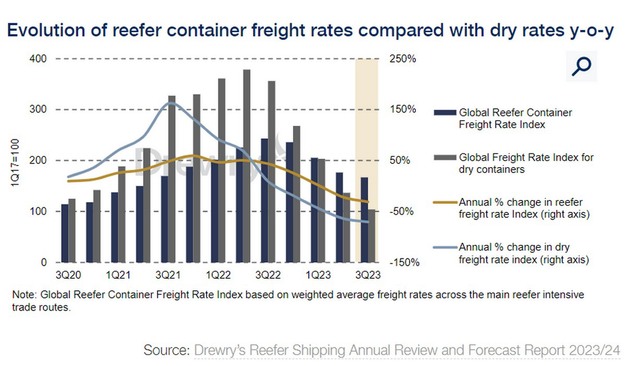

Reefer container freight rates have been declining since their peak of 3Q22 but at a more measured pace than for dry freight. This is because the reefer's peak was less pronounced due to the greater prevalence of annual contracts, while the stronger resilience of the less overtonnaged North-South trade routes, on which the majority of reefer cargo moves, has also helped. Drewry's Global Reefer Container Freight Rate Index, a weighted average of pricing across the top 15 reefer-intensive deep sea trades, declined 22% to $4,840 per 40ft in the year to 2Q23. And initial indications show that the fall will have accelerated to 31% by the third quarter. But despite such corrections, reefer container freight rates remain some 60% above pre-pandemic levels, while pricing for dry cargo has reached parity.

For more information: drewry.co.uk