At the onset of the pandemic, carriers were able to cut capacity in line with the massive demand contraction. However, the same degree of commitment has not been seen with the volume crash in the last 4 months of 2022, with the carriers either not able to, or possibly not willing to. Instead, there has been a wait-and-see approach, where carriers are seemingly waiting for their competitors to blank sailings, before finally blanking themselves. This results in scheduled capacity that changes drastically the closer we get to actual deployment.

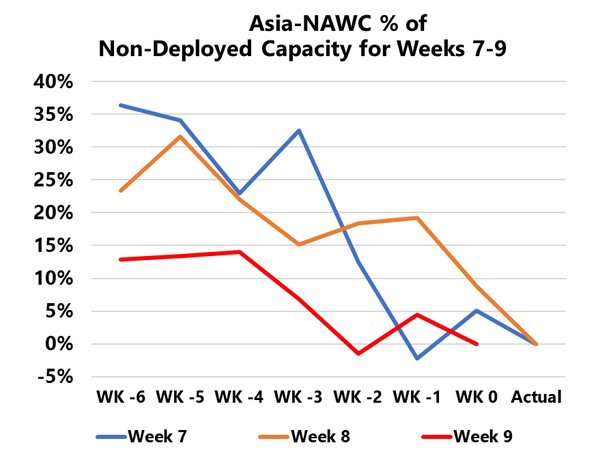

On Asia-North America West Coast, we can see scheduled deployment for Week 7-9 2023, as they were at different points in time (‘Actual’ refers to the actual deployment, ‘Week 0’ refers to the scheduled deployment recorded in the same week as the week being measured i.e. scheduled capacity for Week 7 as recorded in Week 7 etc., ‘-1’ refers to the scheduled deployment one week prior to the week being measured i.e. scheduled capacity for Week 7 as recorded in Week 6, and so on).

Schedules that were only 2 weeks out were somewhat reflective of what the actual deployment eventually turned out to be, whereas schedules even 3 weeks out had roughly 10%-20% of “extra” capacity that did not get deployed. 6 weeks out however, we are looking at an excess scheduled deployment of 20%-40%, except for in Week 9 where it was in excess of 10%-15%.

This means that in the 3 most-recent weeks, carriers have corrected significant amounts of capacity. The same trend was also seen at the end of 2022 after Golden Week, where there was an excess of 60%-80% of capacity that was scheduled but not deployed. On Asia-North America East Coast however, the capacity correction is less frequent, and when it does happen, it is not to the same extent as seen to the West Coast.

For more information: sea-intelligence.com