European physical markets

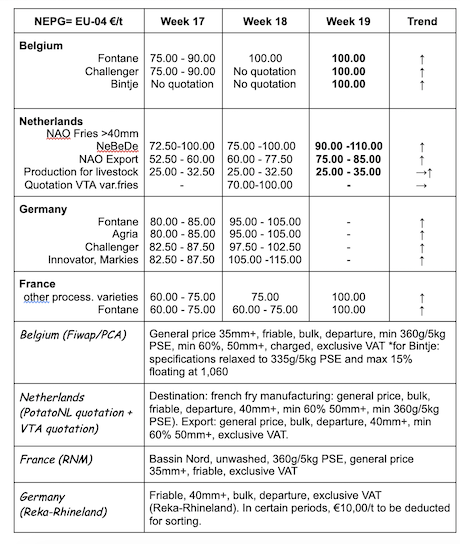

Price summary €/t (source: NEPG):

Belgium

Fiwap/PCA market message:

Potatoes for processing: sustained markets thanks to the demand for processing (several active buyers), and export (to Southern Europe, England, Eastern Europe (including Ukraine)), and due to the weather not being very favorable for the growth of the early varieties. Supply is still limited, especially due to the low free stocks.

Fontane, Bintje and Challenger: around 10.00 €/q for immediate delivery. Higher prices for delayed delivery (June-July).

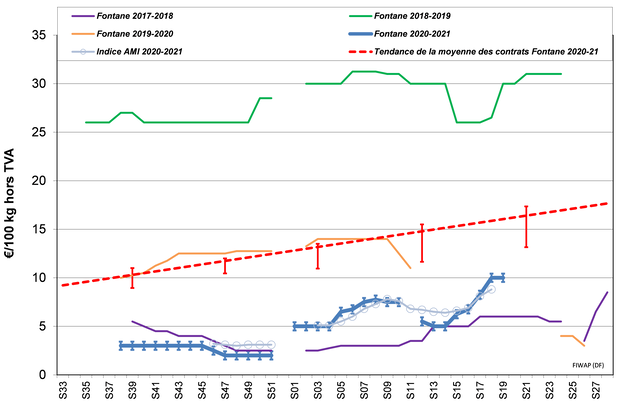

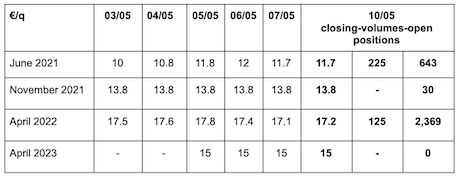

Forward market

EEX in Leipzig (€/q) Bintje, Agria and related var. for transformer, 40 mm+, min 60 % 50 mm +:

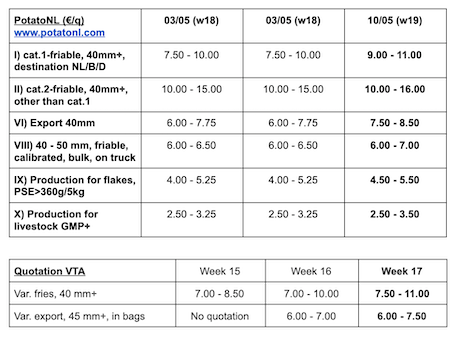

Netherlands

All the quotations were still up and sustained, because of the lower offer (low free volumes in stock, producers’ will to cover the higher storage costs as best as possible), a higher industrial demand (especially from Belgium) after the partial reopening of restaurants, and the weather which is not favorable for the growth of the early varieties. Little change, however, on the fresh markets (neither in price nor in volumes) where the share of imported early potatoes increases on the shelves. Producer prices from 12.00 to 24.00 €/q for firm flesh and from 8.00 to 15.00 €/q for soft flesh. In export, Spain and England buy the Agria/Markies varieties on a basis of 14.00 - 18.00 €/q at the producer. The lesser quality is sought after by Ukraine, Romania and Africa at 10.00 - 13.00 €/q, calibrated in bags or big-bags.

France

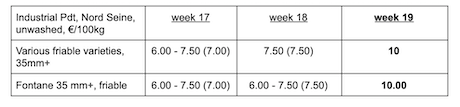

Industrial production, bulk, departure, excl.VAT, Nord-Seine, €/qt, min - max (moy)(RNM):

Purchases from the industry are intensifying depending on each case (finished products in stock or not), and prices are up. Intermediate trade remains very present as well, at higher prices (who is buying?). No delay in removal of contracts. In export, the end of the campaign is being felt, but the volumes and prices are regular for the friable quality and there are significant gaps depending on variety and quality. Italy is not very present, neither is Eastern Europe. In the fields, on May 5th, planting (all regions combined) was estimated at 98% and emergence is slow. Irrigation is in place in the Centre/Beauce, and in the Grand-Est/Champagne, especially to allow ridging.

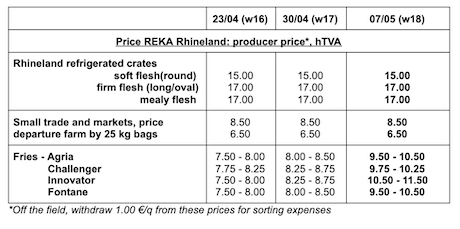

Germany

Fresh market unchanged: prices for firm flesh at 10.83 €/q and for soft/mealy flesh at 10.25 €/q. But the merchandise from refrigerated crates-pallets is 3€ higher (see REKA prices in table below!).

Processing market: very firm and rising prices: 10.50 - 11.50 €/q for Innovator/Markies (8.25 - 8.75 €/q last week). Agria at 9.50 - 10.50 €/q (8.00 - 8.50 €/q), Challenger 9.75 - 10.25 (8.25 - 8.75 €/q last week) and Fontane at 9.50 - 10.50 €/q (8.00 - 8.50 €/q). As vaccination progresses and lockdown is being partially lifted, markets are all revived again. Varieties for chips/crisps are firm with a new increase, and prices vary between 11.00 and 15.00 €/q.

Potatoes for livestock: higher prices, between 1.00 and 3.00 €/qt.

Native early potatoes: in some cases, it took 7 weeks for the potatoes to emerge. In 2020, the regional media was celebrating the very first shoots on May 2nd, but this year, they are not expected until May 17th. There will be a significant difference between the crops with and without tarps.

Imported early potatoes: Egypt origin around 50.00 €/q. Israel, especially the “Drillinge” potatoes, up to 62 - 70 €/qt, thanks to the high demand from countries like Italy or Spain who normally do not buy, or only very little!

Organic potatoes: unchanged producer prices at 40.00 €/q (all varieties and markets combined), returned trade.

Great Britain

Average price free market for the week ending on May 4th, 2021: 14.01 £/q (15.26 £/q last week), i.e. +/- 16.30 €/q. Prices are down, especially because the quotation basket contained more basic varieties last week, compared to this week.

On the wholesale markets, the prices for Markies and Agria in bags keep going up this week, around 18.50 - 21.00 €/q (calibrated departure) for the superior quality. The lesser quality remains at 6.00 - 9.50 €/q and has few buyers. Most of the trade is waiting for a change in the governmental measures decided on May 10th, hoping for a notable lift of the lockdown.

In the fields, the beginning of the week was cold with some snow, which interrupted the planting for some. The temperatures on the ground were colder than desired. However, the subsequent nicer weather allowed for some good progress.

For more information:

FIWAP

www.fiwap.be